Generate Promissory Note

A promissory note is a legal document that sets out the details of a loan made between two people, a borrower and a lender. It outlines the borrower's promise to repay the lender within a specified time.

Start your Promissory Note

Answer a few simple questions to generate your document.Last Updated January 2026

What is a Promissory Note?

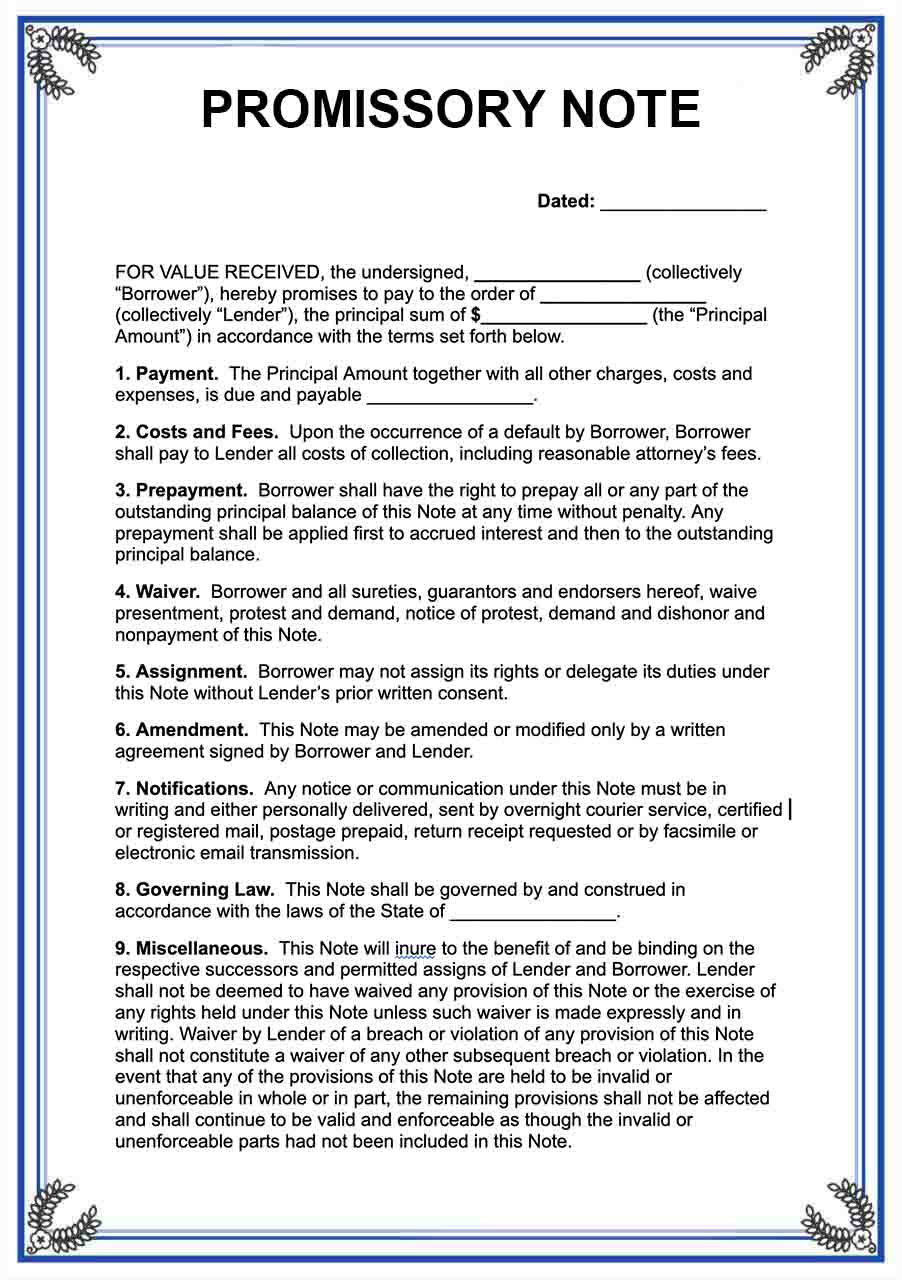

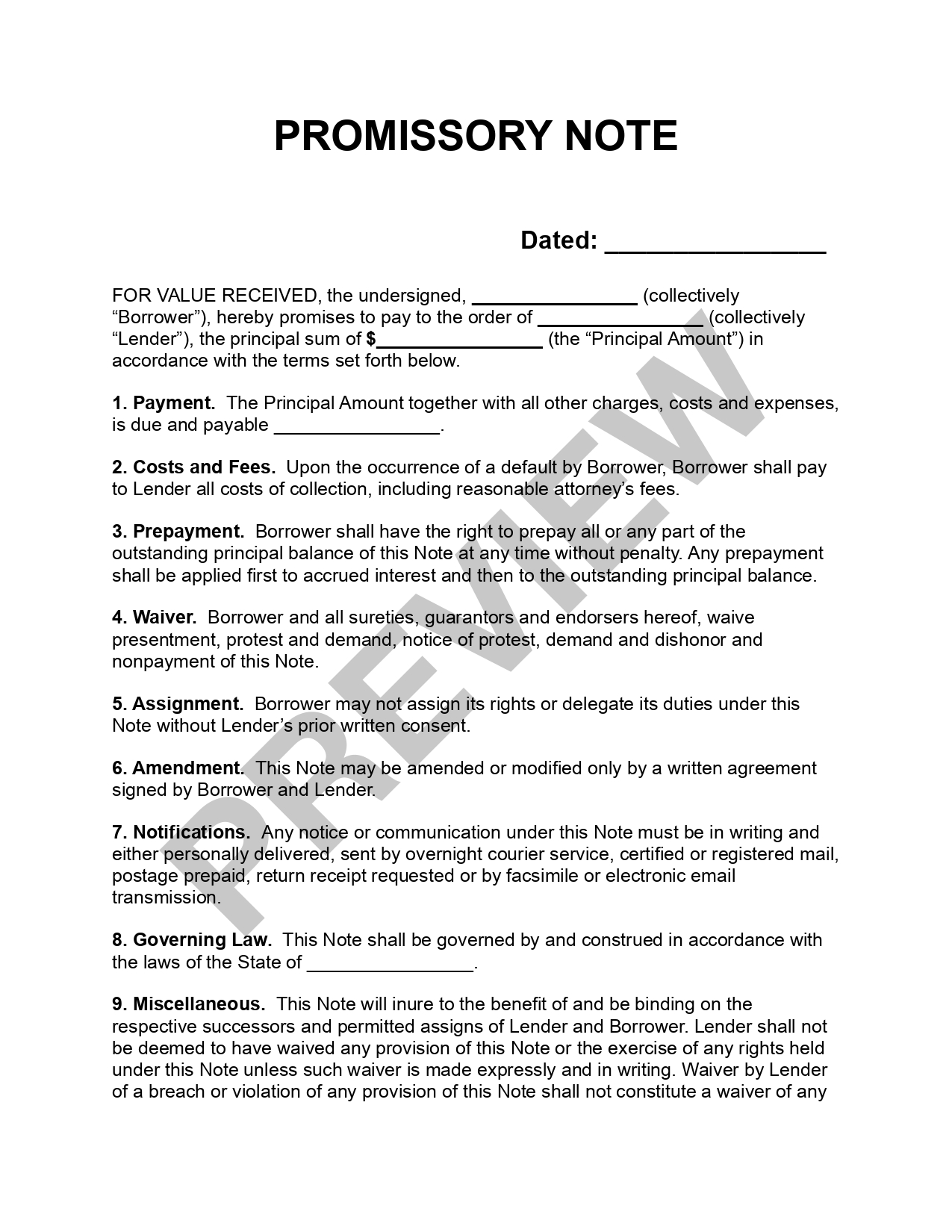

A promissory note is a legal document that sets out the details of a loan made between two people, a borrower and a lender. The note clearly outlines the borrower's promise to fully repay the lender within a specified amount of time. It includes all the terms and conditions of the loan transaction and ensures the parties have a thorough and complete written record of the deal and their intentions. As such, the note should be finalized before any money changes hands. The document also acts as a formal record of the transaction.

Types of Promissory Notes

There are several types of promissory notes used for different kinds of loan arrangements:

-

Simple Promissory Note: The most basic form that outlines the loan amount, interest rate, and repayment terms without complex conditions.

-

Demand Promissory Note: Allows the lender to demand repayment at any time, rather than having a fixed maturity date.

-

Installment Promissory Note: Requires the borrower to repay the loan in regular installments, typically monthly, over a set period.

-

Secured Promissory Note: Backed by collateral, meaning if the borrower defaults, the lender can seize the specified assets.

-

Unsecured Promissory Note: Not backed by collateral and relies solely on the borrower's promise to repay.

Who needs a Promissory Note?

A promissory note may be needed in many circumstances. Here are some common situations:

-

Personal loans between friends or family: To formalize lending money to someone you know and protect both parties.

-

Business loans: When a business borrows money from investors or other parties outside of traditional banking.

-

Real estate transactions: Often used in real estate deals to document seller financing or bridge loans.

-

Student loans: Used by educational institutions to document money lent to students.

What should I include in my Promissory Note?

Key elements that you should include in your Promissory Note:

-

Lender and Borrower Information: Full legal names and contact information for both parties.

-

Principal Amount: The amount of money being lent.

-

Interest Rate: The rate of interest charged on the loan, if any.

-

Repayment Terms: How and when the loan will be repaid (installments, lump sum, etc.).

-

Late Fees: Any fees charged if payments are not made on time.

-

Governing Law: The state whose laws will govern the note.

-

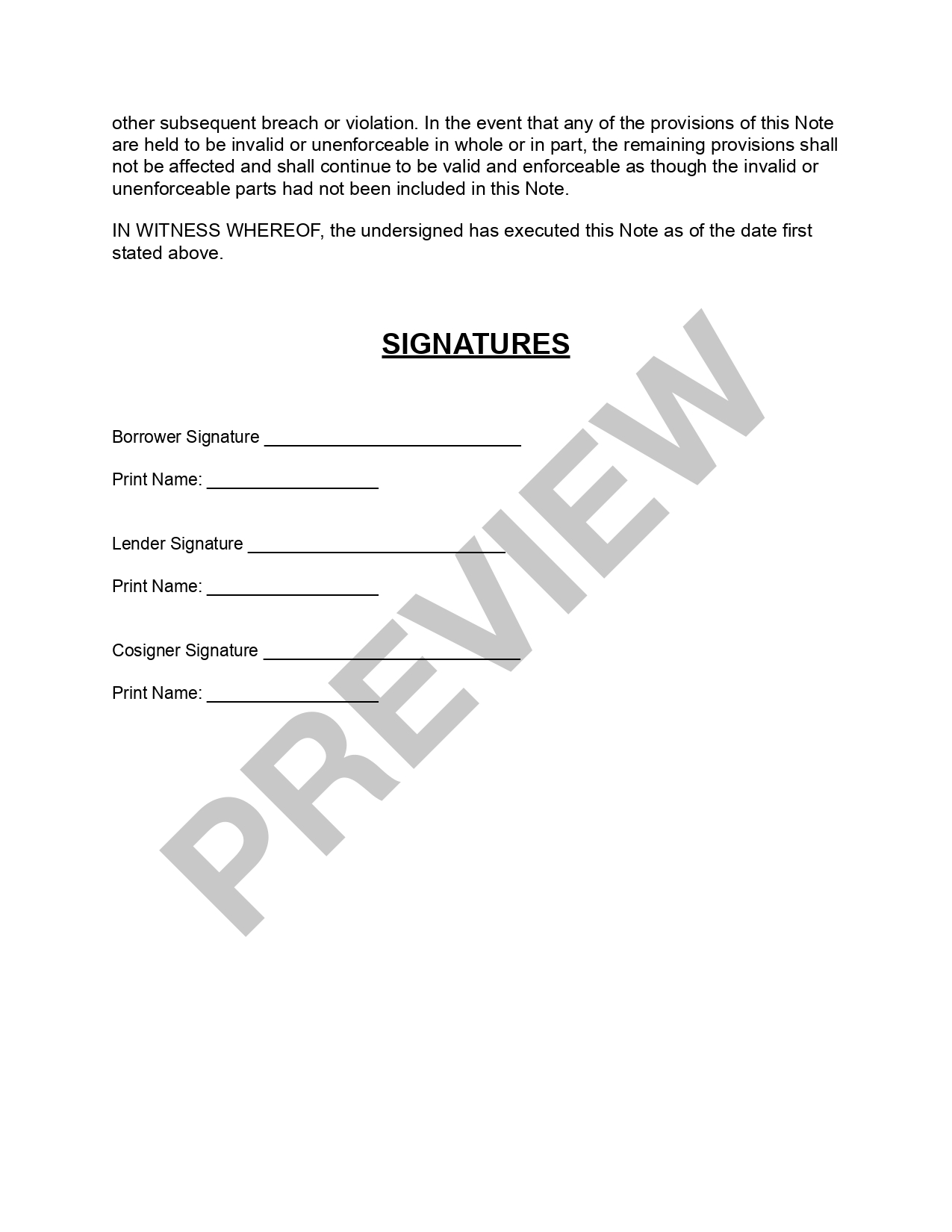

Signatures: Signed and dated by both the lender and borrower.

Frequently Asked Questions

Yes, a promissory note is legally binding once it is signed by both the borrower and lender. It represents a formal promise to repay the debt and can be enforced in a court of law. The specific requirements for a promissory note to be legally enforceable may vary by state.

A promissory note is a simpler document that contains a borrower's promise to repay a specific amount. A loan agreement is more comprehensive and includes detailed terms and conditions for both parties. Promissory notes are typically used for smaller, simpler loans while loan agreements are used for larger or more complex transactions.

In most cases, a promissory note does not need to be notarized to be legally enforceable. However, having it notarized adds an extra layer of authenticity and can be useful if the document is ever contested in court. Check your state's specific requirements as laws may vary.

If a borrower defaults on a promissory note, the lender has several options: they can demand immediate payment of the full amount (if an acceleration clause is included), take legal action in court to recover the debt, or, if the note is secured, seize the collateral. The lender should document all default-related communications and consult with a legal professional.

A cosigner or guarantor is a third party who agrees to be legally responsible for repaying the loan if the borrower cannot. This provides additional security for the lender. A cosigner or guarantor is optional but may be required if the borrower has questionable financial standing or credit history.